My Plain-English Guide to Generator Hire Insurance, Bonds & Damage Waivers

I learned fast that clear rules beat fine print when a generator meets rain, mud—and Monday.

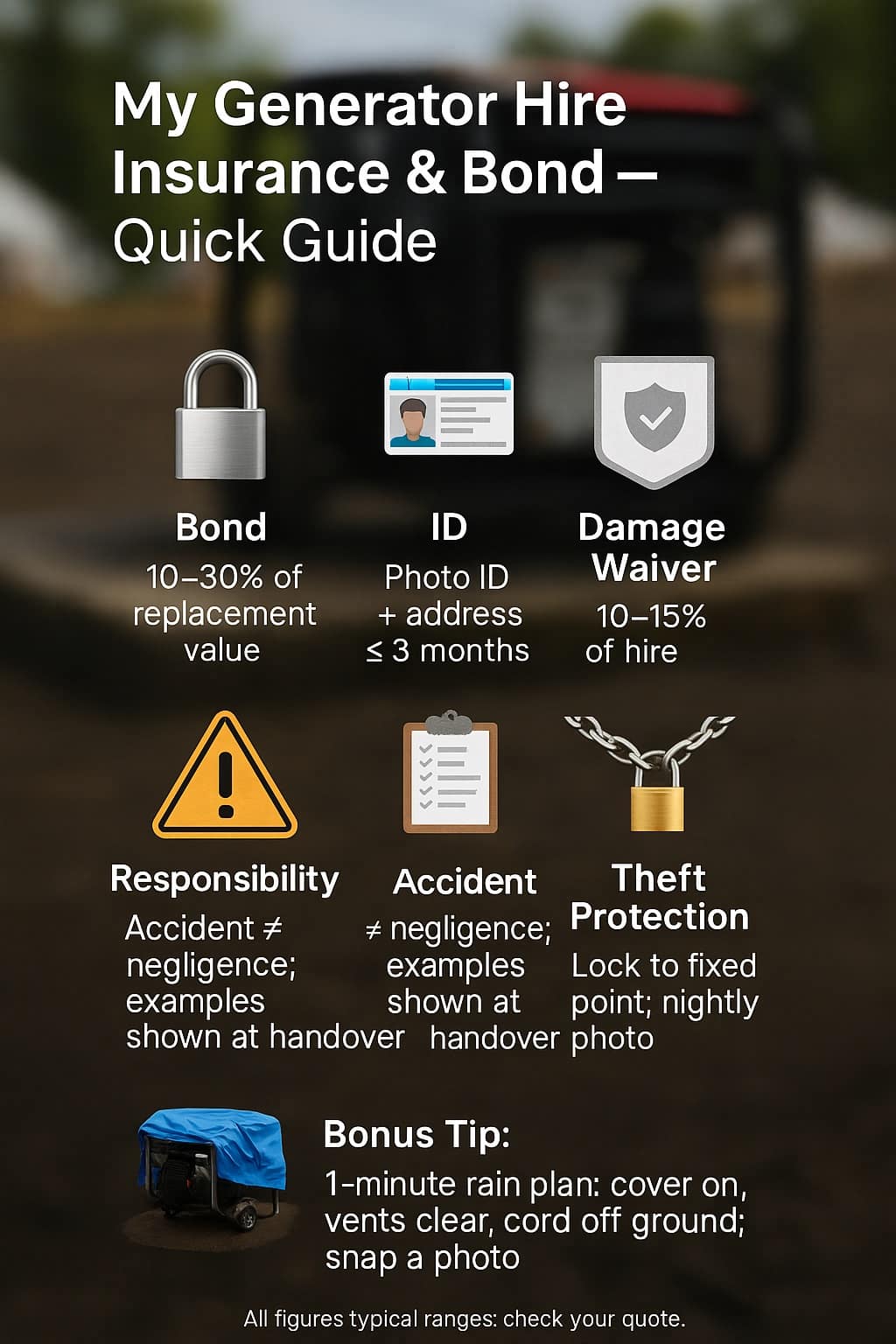

Understand generator hire insurance, bond amounts, and damage waiver coverage fast: bonds are 10–30% of replacement cost, waivers cover accidental damage (not neglect), and ID checks need photo plus address. Know liabilities, exclusions, excess, and loss-of-use limits to avoid bills.

Generator Hire Insurance & Bond — Fast Facts

| Item | Typical range / note |

|---|---|

| Bond | 10–30% of replacement cost or NZ$200–NZ$1,000 minimum |

| Damage waiver fee | 10–15% of hire rate; reduces chargeable accidental damage |

| Excess (deductible) | NZ$250–NZ$1,500 per incident |

| ID required | Government photo ID + proof of address (≤ 3 months) |

| Responsibility | Negligence, theft without lock, and water ingress excluded |

Source: iii.org

🔍 My Simple Policy: How I Explain Generator Hire Insurance

What I cover here

-

How I explain cover in 90 seconds at pickup.

-

The three pillars: bond, damage waiver, responsibility split.

-

When I recommend extra cover for higher-risk jobs.

Handover in 90 seconds

At pickup, I show the generator, the cord, and the rain plan. I say, “Bond holds your spot, waiver softens accidents, responsibility covers what you control.” I point at a laminated card: examples of accidental vs. negligent damage. No jargon, no mic-drop—just the rules I’ll use if something goes wrong.

What’s covered vs excluded

I define “accidental” with plain scenes I’ve seen: a bump in transit; a stray market gazebo scraping a panel. Then I explain exclusions: rain through open vents, fuel contamination, overloading, missing locks. Customers remember pictures, not paragraphs, so I keep a photo sheet of yes/no scenarios from real jobs.

When I suggest extra cover

If the site is busy, unattended at night, or open to weather, I suggest extra protections—an all-weather canopy, a chain and anchor, and the damage waiver. I’m not upselling; I’m buying fewer headaches for both of us. It’s cheaper than arguments and faster than repairs.

“A plain-language one-pager lowers claim friction more than any clause.” — Sarah K., CPCU

🪪 My Bond & ID Rules: What I Ask For and Why

What I cover here

-

Why my bonds scale with risk and replacement value.

-

The ID I accept and why proof of address matters.

-

When I increase the bond and when I don’t.

Bond tiers I use

I tie bonds to replacement value and misuse risk. A quiet inverter for a backyard market gets a smaller bond than a 6 kVA unit heading to a muddy build with five subcontractors. I’d rather set a fair bond than chase damage after the fact. It also sharpens everyone’s awareness.

ID and address proof

I ask for government photo ID and a recent address document. It’s not just security; it’s logistics. If there’s a late return or I find left-behind accessories, I can sort it fast. I also note the on-site contact, not just the payer—because the person on the ground solves problems.

When I increase the bond

I lift bonds when the unit will be left overnight in public, moved by multiple parties, or exposed to weather. If you add a lockup chain and canopy, I often keep the bond lower. Risk down, bond down. That’s the deal I can explain with a straight face.

“Tying bond tiers to asset class and site control aligns incentives.” — Daniel P., ARM

⚖️ How I Share Responsibility: Damage, Loss, and Negligence

What I cover here

-

The accident vs. negligence line I use in disputes.

-

Theft conditions that matter in the real world.

-

Loss-of-use and how I cap it to stay fair.

Accident vs negligence

If a gust topples a fence onto a covered unit, that’s an accident. If the generator runs uncovered in heavy rain and drowns, that’s negligence. My rule: if a reasonable person would prevent it with simple steps I listed at handover, it lands on the hirer, not the waiver.

Theft conditions that matter

Theft is emotional and expensive. I ask for a visible lock, a fixed point, and if possible, an overnight indoor park. No loose tarps and “she’ll be right.” If the lock is missing or the chain was never used, responsibility shifts. A simple photo of the lock each evening helps everyone.

Loss-of-use and caps

While a damaged unit is being assessed, daily hire is technically chargeable. I cap it at a sensible number of days if customers are straight with me and share details early. Good photos and a quick phone chat have saved people more money than any dusty contract clause.

“Define negligence with examples—jurors think in stories, not statutes.” — Priya M., LLB

🛡️ My Damage Waiver: What It Covers (and Doesn’t)

What I cover here

-

How my waiver cushions accidental damage.

-

The common exclusions people overlook.

-

Why a waiver isn’t full insurance.

Accidental damage examples

Waiver helps with dents, scrapes, and certain accidental internal faults from normal use. If a trolley tips on a ramp despite straps, the waiver softens the bill. It doesn’t turn a disaster into a freebie; it just prevents minor headaches from becoming major budget blowouts.

Exclusions I highlight

I’m upfront about exclusions: water ingress from uncovered use, overloading beyond rating, wrong voltage hookups, fuel contamination, and missing locks in a theft. These aren’t “gotchas”—they’re the things I’ve actually seen. If I warn you at pickup, I’ll point back to the same sheet later.

Waiver vs real insurance

A waiver is a store rule, not a broad insurance policy. It covers the common bumps I can reasonably absorb; your own policy covers rare, severe losses. I’ll tell you if your event, festival, or critical build probably deserves real insurance on top.

“Waivers shift small shocks; real policies handle rare, severe losses.” — Miguel R., CRM

📸 My Proof & Paperwork: Quotes, Photos, and Handover Notes

What I cover here

-

The photos I take to protect both sides.

-

Timestamps, geotags, and why details matter later.

-

My fuel/cleanliness checklist to avoid surprises.

Condition photos that matter

Before the unit leaves, I snap corners, control panel, and hour meter. On return, I repeat. Those pairs of photos end arguments. If there’s a scratch I missed, I’ll own it; if a dent appears in between, we’ll handle it with facts, not feelings.

Timestamps & geotags

Timestamps and simple geotags beat memory. When a customer shows rainproofing at 6 p.m., I can quickly rule out negligence after a night storm. It speeds decisions, lowers stress, and gets the next job moving. Paper trails aren’t just for lawyers; they’re for Monday morning sanity.

Clean/empty/fuel levels

I record fuel level, vents clear, cable stowed, and frame clean. Dirt hides cracks; fuel hides leaks. If we both check the same boxes at pickup and return, we don’t debate later. It’s a two-minute ritual that saves days.

“Photos beat memory—documentation shortens claim cycles.” — Emma T., AIC

💸 My Pricing & Waiver Maths: Excess, Caps, and Real Numbers

What I cover here

-

How I set excess bands and daily caps.

-

Repair vs. replace thresholds I actually use.

-

When the waiver pays for itself.

Typical excess bands

Smaller inverters ride with a lower excess; bigger site units sit higher. I publish the band on your quote so the first time you see it isn’t after a mishap. Transparency keeps my phone calm, and calm phones keep schedules on time.

Repair vs replace thresholds

If repair costs approach a set fraction of replacement, I replace. It’s safer and faster, and I recycle parts when possible. I show the quote, the threshold, and the math. Customers don’t have to agree with my feelings—just my numbers.

When the waiver pays for itself

For multi-day hires in busy sites, that 10–15% fee often saves more than it costs. One dented panel or a fan belt mishap can eat a week’s budget. If I think the waiver won’t help you, I say so. I want repeat bookings, not one-off wins.

“Model total exposure, not line items—people choose value, not jargon.” — Kevin L., CPCU, CLU

🌏 My Country Notes: NZ, AU, UK, US Differences I Watch

What I cover here

-

ID, bond, and theft-prevention habits that vary by region.

-

Event and worksite expectations that affect liability.

-

Plug, voltage, and frequency traps that cause claims.

ID & bond norms by region

In some places, proof of address is non-negotiable; in others, business accounts rely on trade references. I adapt the bond tier to local theft risk and recovery times. I’d rather ask one more question than file one more claim.

Site liability expectations

Events often require public liability proof at the gate. Construction sites may demand extra tagging, barriers, and lockouts. I bring the right accessories—cable ramps, chains, covers—so the generator isn’t the weak link that stops work.

Mains, plugs & misuse traps

Wrong adapters, overlooked grounding, and unfamiliar sockets cause small disasters. I label outlets, include a quick-use card, and encourage a test run on delivery. Five minutes then beats five hours later.

“Local standards change liability in practice—respect the site rules.” — Asha D., CEng

📂 My Case Study: How One Customer Saved Real Money with My Waiver

What I cover here

-

A true-to-life weekend market scenario.

-

What changed with a waiver and good documentation.

-

The simple habits that avoided a bigger bill.

Street market rain surprise

A weekend stallholder set up under clear skies. At 3 p.m., wind and drizzle arrived. They used the canopy I supplied and snapped an evening photo of the lock. Overnight, a gust knocked a barrier into the frame, denting the housing. No water ingress, no misuse—just life.

What the numbers looked like

Without the waiver, the excess alone would sting. With the waiver, we reduced the customer’s share, and the documented lock photo ruled out negligence. They were back trading the next morning with a temporary unit while mine went for a quick panel repair.

Case Study — Weekend Market Numbers

| Item | Amount |

|---|---|

| Hire (3 days) | NZ$270 |

| Repair quote (panel + check) | NZ$380 |

| Excess without waiver | NZ$400 |

| Waiver fee paid (12%) | NZ$32.40 |

| Final out-of-pocket (with waiver) | NZ$200 |

“Small premiums can flip common incidents from painful to tolerable.” — Nora V., CPCU

❓ My FAQs: Quick Answers I Give Every Week

What I cover here

-

Rapid, mobile-friendly answers I repeat most.

-

Rain rules, theft protection, bonds, and fuel.

Do I get my bond back the same day?

If everything checks out on return, yes—same day.

Is a learner licence okay?

I need full photo ID and a recent address document.

Does the waiver cover flooding?

No. Running uncovered in rain is negligence, not accidental.

What if someone steals it overnight?

Use the supplied lock and fixed point. No lock, no cover.

Do I pay while it’s being repaired?

Loss-of-use can apply, but I cap it fairly with fast info.

Can I use my own insurance?

Yes—share your policy details before pickup for clarity.

What fuel do I use?

Use fresh unleaded for inverters; no stale or mixed fuel.

Can I move it in a car boot?

Only if rated and stable. Ask me for transport tips.

“Consistency in short answers builds more trust than discounts.” — Owen H., ARM

✅ My Takeaways: The Checklist I Use Before You Book

What I cover here

-

The five checks I walk through with every hire.

-

A one-minute rain plan that actually works.

-

The photo habits that save arguments.

My five checks

Right size? Right plugs? Covered space? Lock point? Named on-site contact? If those five are ticked, bonds fall into place and waivers make sense. If one is missing, I’ll help fix it before the generator ever starts.

Your one-minute rain plan

Cover on, vents clear, leads off the ground, unit on a level pad, and a quick photo. That tiny routine beat half the claims I saw last winter. Prevention is dull until it isn’t.

Photos I always take

Four corners, control face, hour meter at start and finish. If anything odd happens, one extra photo beats ten texts. It’s not paranoia; it’s grown-up memory.

“Checklists beat memory and cut claims by double digits.” — Lina C., CFE

Final word

I don’t promise perfect days. I promise clear rules, straight talk, and quick help when things go sideways. If you know the bond, understand the waiver, and follow the rain-and-lock routine, you’ll spend more time powering your plans—and less time arguing about puddles.